Lifestyle

6 Bank Fees You Can Get Waived Just by Asking

By Erica Coleman · June 25, 2026

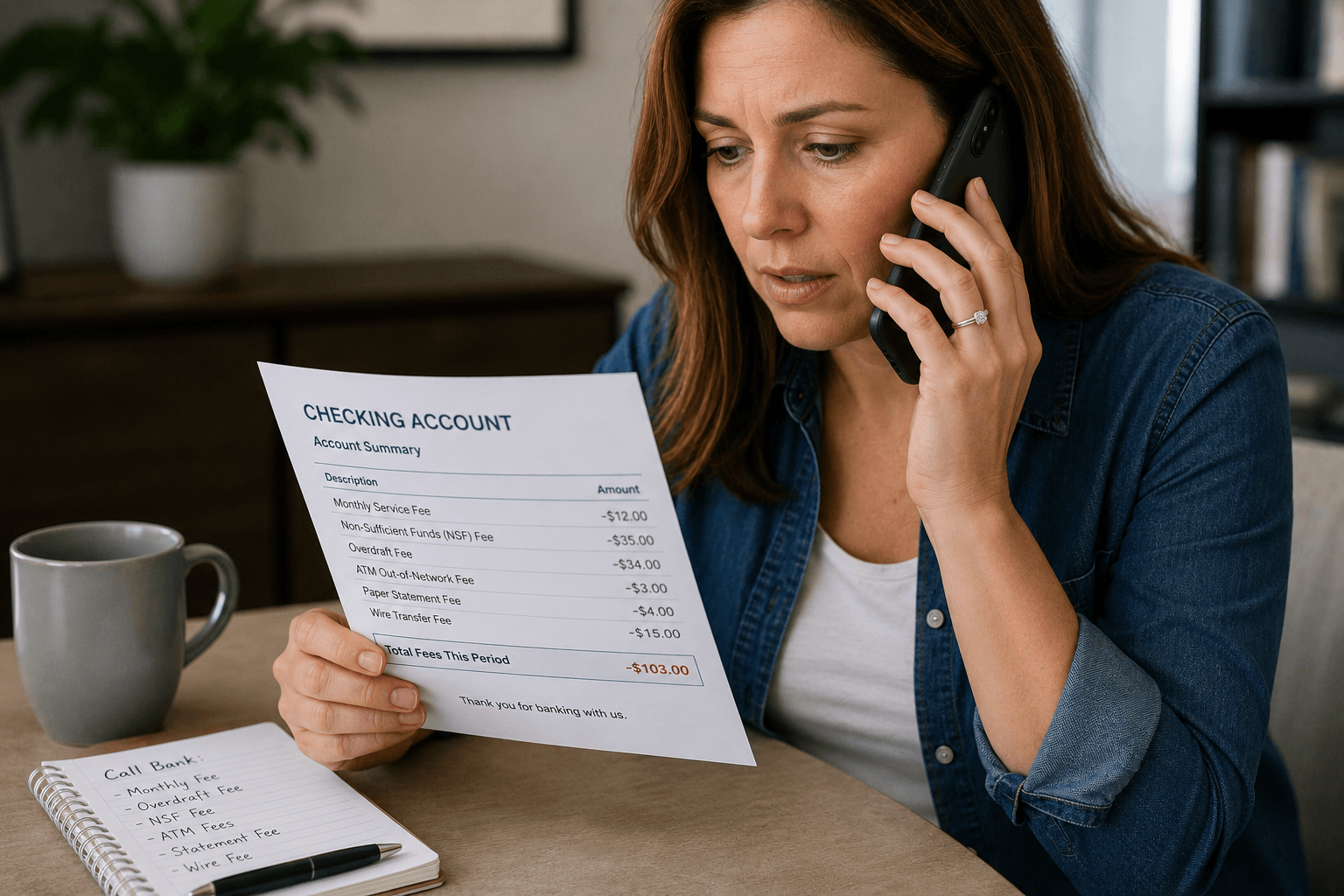

American banks collected approximately $7.7 billion in overdraft and insufficient funds fees alone in 2023, according to the CFPB. Add maintenance fees, ATM fees, wire transfer fees, and paper statement fees and the total is significantly higher. Many of these charges are waivable — but only if you ask. Banks are not in the business of volunteering to reduce their revenue. Here are six fees worth a phone call.

1. Monthly maintenance fee

Most checking accounts charge $10 to $15 per month unless you meet a minimum balance or set up direct deposit. That’s $120 to $180 per year for the privilege of keeping your money in their vault. Call and ask whether the fee can be waived based on your account history, your relationship with the bank, or by meeting an alternative requirement you weren’t aware of. If they won’t waive it, ask to be switched to a no-fee account — most banks have one and most customers don’t know it exists.

2. Overdraft fee

Overdraft fees average $26 to $35 per incident. If you overdraft once due to a timing issue — a payment cleared before your paycheck deposited — call and ask for a courtesy reversal. Most banks allow at least one per year for customers in good standing. Some allow more. The key phrase: “I’d like to request a courtesy reversal of this overdraft fee.” If the first representative says no, ask to speak to a supervisor. The fee reversal authority often sits one level above the front line.

3. ATM fees — both yours and the other bank’s

Using an out-of-network ATM typically triggers two fees: one from your bank ($2-$3) and one from the ATM owner ($2-$5). Your bank’s fee is the one you can challenge. Call and ask whether your account type qualifies for ATM fee rebates — several banks reimburse a set number of out-of-network ATM fees per month. If yours doesn’t, ask whether upgrading to a different account type would include that benefit.

4. Wire transfer fee

Domestic wire transfers typically cost $15 to $30. International wires cost $35 to $50. If you wire money regularly — for real estate closings, business payments, or family support — ask whether the fee can be reduced or waived based on your account balance or relationship. Many banks waive wire fees for customers who maintain a threshold balance. The threshold is rarely posted publicly. You have to ask.

5. Paper statement fee

Some banks charge $2 to $5 per month for mailing a paper statement — a fee that exists specifically to push customers toward paperless billing. If you prefer paper statements, call and ask for the fee to be waived. If you don’t care about paper, switch to electronic delivery and the fee disappears. Either way, you shouldn’t be paying $24 to $60 per year for a printout of information you can access online for free.

6. Account closure fee

Some banks charge $25 to $50 if you close an account within 90 to 180 days of opening it. If you’re closing an account because of poor service or unexpected fees, ask the representative to waive the closure fee as a customer retention gesture. If they won’t waive it, wait until the early closure window expires — then close. The fee is designed to lock you in. Knowing the timeline gives you the leverage to avoid it.

The single most effective sentence in bank fee negotiations: “I’ve been a customer for [X] years and I’d like this fee waived.” Length of relationship is the strongest card you hold. Banks spend significant money acquiring new customers and prefer to keep existing ones — even at the cost of a $35 fee reversal.