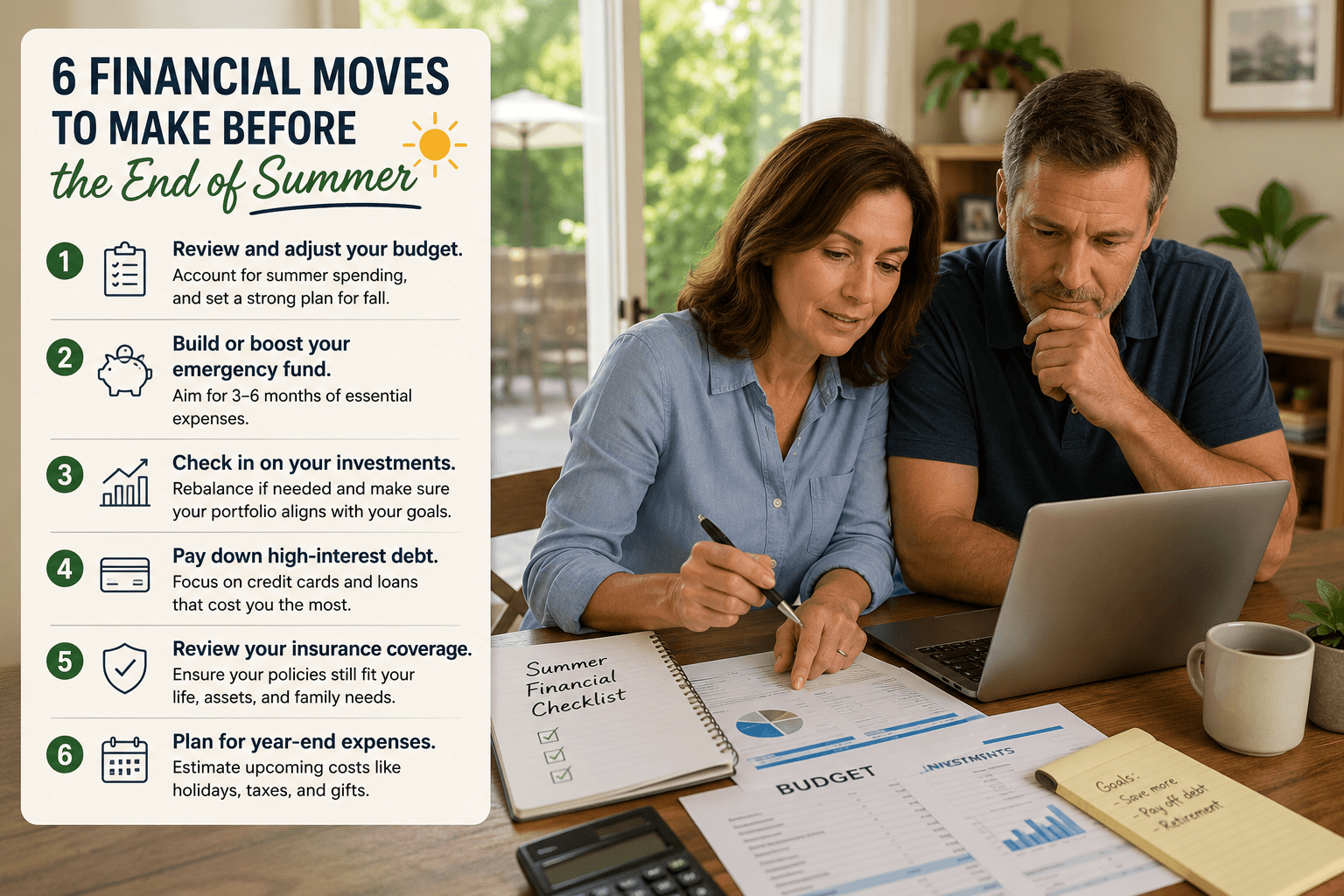

Lifestyle

6 Financial Moves to Make Before the End of Summer

By Curtis Jones · July 5, 2026

Summer is when financial attention drifts. Vacations, cookouts, and longer days push budgets and planning to the back of the mind. Financial advisors say the six tasks below are the ones most commonly deferred from spring to “after summer” — and the ones that cost the most when they’re pushed to fall.

1. Review your tax withholding

If you owed a large amount at tax time or received a huge refund, your withholding is wrong. Use the IRS Tax Withholding Estimator at irs.gov to check whether your current paycheck withholding matches your projected tax liability. Adjusting now — rather than in December — gives the adjustment time to take effect across the remaining pay periods.

2. Max out your HSA if you have one

Health Savings Account contributions for 2026 are capped at $4,300 for individuals and $8,550 for families. HSA contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses — a triple tax advantage no other account offers. If you haven’t maxed out your contributions for the year, increasing your payroll deduction now spreads the remaining amount across the second half of the year.

3. Check your credit report

You’re entitled to one free credit report per year from each of the three major bureaus at annualcreditreport.com. If you haven’t pulled yours this year, do it now. Review it for errors — incorrect accounts, wrong balances, or accounts you don’t recognize. Disputing an error takes 30 days to resolve, and catching it now rather than in October means it’s corrected before you apply for any fall financing.

4. Review your insurance coverage

If you’ve made changes to your home, added a vehicle, or experienced a life event since your last policy renewal, your coverage may not reflect your current situation. Call your auto, home, and umbrella insurance agents and ask whether your coverage is adequate and whether any new discounts apply. A 15-minute call often produces savings or identifies gaps before a claim forces the discovery.

5. Set your open enrollment calendar reminder

Medicare open enrollment runs October 15 through December 7. Employer open enrollment varies but typically falls between October and November. Set a calendar reminder for two weeks before your enrollment window opens — with a note to compare plans rather than auto-renewing. The plan that was cheapest last year may not be cheapest this year.

6. Build or replenish your emergency fund

Summer spending — vacations, camps, home projects — often drains savings. If your emergency fund has dropped below three months of expenses, use the remaining summer to rebuild it before the fall brings its own demands. Even $100 per paycheck into a dedicated savings account adds $800 to $1,000 by October.

Eight weeks is enough time to address all six. None requires more than an afternoon. The financial version of “I’ll do it after summer” almost always becomes “I’ll do it after the holidays” — which becomes next year.