Lifestyle

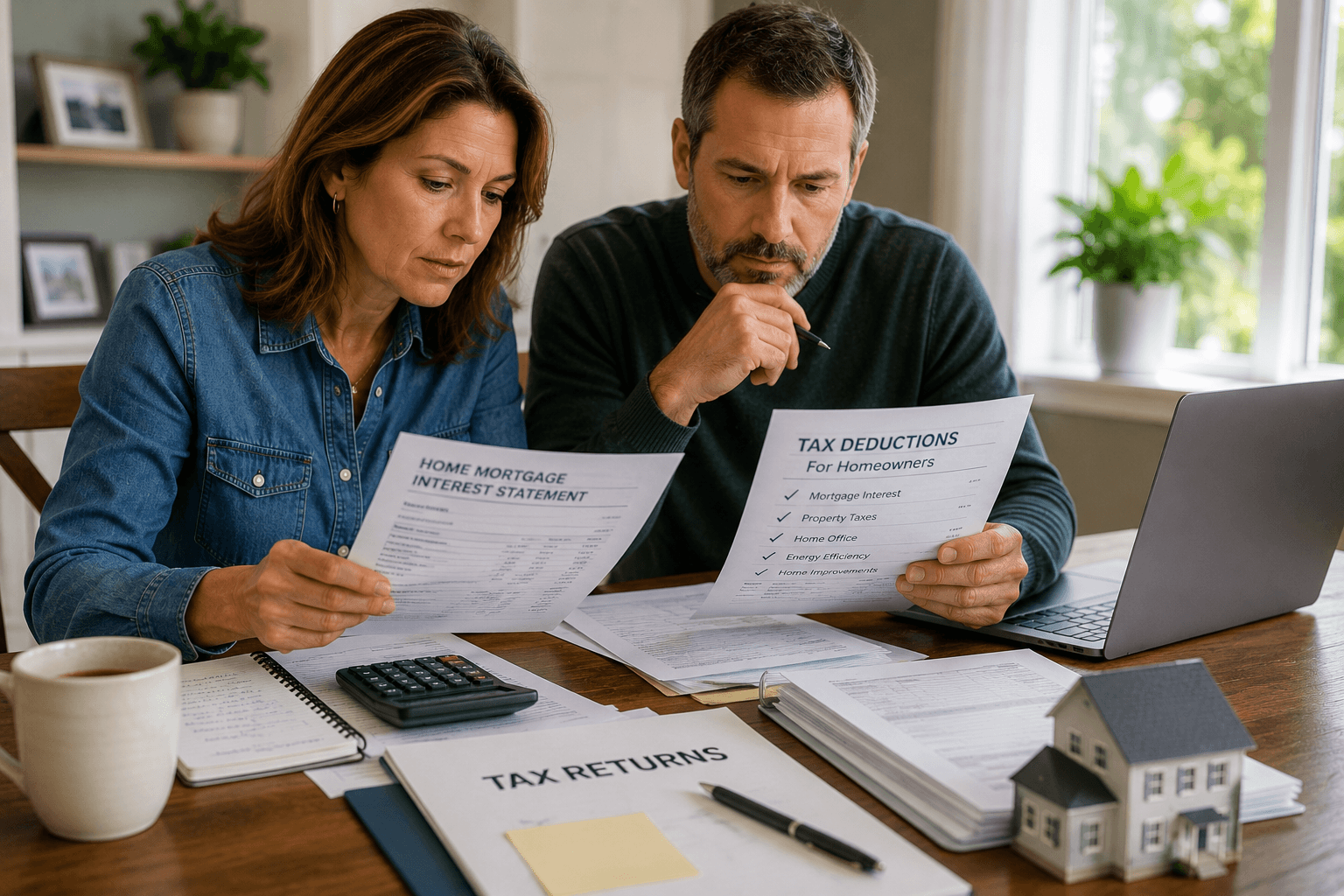

5 Tax Deductions Most Homeowners Miss Every Year

By Erica Coleman · June 27, 2026

The standard deduction is $15,700 for single filers and $31,400 for married couples filing jointly in 2026. Many homeowners take the standard deduction because they assume they can’t beat it. CPAs say a significant number of them are wrong — because they’re not counting everything they’re entitled to.

1. Mortgage interest — including on a second home

You can deduct mortgage interest on up to $750,000 of mortgage debt ($375,000 if married filing separately). This includes your primary residence and one additional home — a vacation house, a condo, even a boat with sleeping quarters. Your lender sends Form 1098 each January showing how much interest you paid. If your mortgage is over $200,000, this deduction alone can push you past the standard deduction threshold.

2. Property taxes — up to $10,000

State and local property taxes are deductible up to $10,000 ($5,000 if married filing separately) under the SALT cap. This is well known but frequently undercounted — many homeowners deduct only the amount on their main tax bill and miss supplemental assessments, special improvement district charges, and school district levies that are also deductible property taxes.

3. Home office deduction — even for part-time use

If you use a dedicated space in your home regularly and exclusively for business — including self-employment, freelance work, or a side business — you may qualify for the home office deduction. The simplified method allows $5 per square foot up to 300 square feet ($1,500 maximum). The regular method deducts actual expenses proportional to the office’s percentage of your home’s total square footage. Many people who work from home part-time don’t realize they qualify.

4. Energy efficiency improvements

The Inflation Reduction Act’s residential energy credits remain available through 2032. If you installed solar panels, a heat pump, insulation, energy-efficient windows, or an electric vehicle charger in 2025 or 2026, you may be eligible for a tax credit of up to 30% of the cost. Credits are better than deductions — they reduce your tax bill dollar for dollar rather than reducing your taxable income. Many homeowners who made qualifying improvements don’t claim the credit because they don’t know it exists.

5. Points paid on your mortgage — the year you bought

If you paid points (prepaid interest) when you took out or refinanced your mortgage, those points are deductible. On a purchase mortgage, the full amount is deductible in the year you paid them. On a refinance, they’re deductible over the life of the loan. A single point on a $400,000 mortgage is $4,000 — a significant deduction that many first-time homebuyers miss in their first year of ownership.

The only way to know whether itemizing beats the standard deduction is to run both calculations. Many tax preparation programs do this automatically. If yours doesn’t — or if you file by hand — add up your mortgage interest, property taxes, state income taxes, and charitable contributions before defaulting to the standard deduction. The 10 minutes it takes could save you hundreds.