Lifestyle

5 Warranties That Are Almost Always a Waste of Money

By Mike Harper · June 27, 2026

Extended warranties and protection plans generate enormous profit margins for the companies that sell them — which is exactly why they’re pushed so aggressively at checkout. The business model depends on most buyers never filing a claim. Here are five warranties where the math almost never works in the consumer’s favor.

1. Extended warranties on appliances

Major appliances — refrigerators, dishwashers, washers, dryers — typically come with a one-year manufacturer warranty. Retailers push extended warranties for $100 to $300 that add two to three years of coverage. The problem: most appliance failures occur either within the manufacturer warranty period or after the extended warranty has expired. The window of coverage the extended warranty actually adds is the window when failures are least likely. Your money is better saved in an emergency fund.

2. Cell phone insurance from your carrier

Carrier-sold phone insurance costs $12 to $17 per month with a deductible of $99 to $275 per claim. Over a two-year phone cycle, you pay $288 to $408 in premiums before you ever break a screen. A quality case costs $30. Many credit cards include phone protection if you pay your monthly bill with the card. The carrier insurance is the most expensive way to protect a phone.

3. Extended car warranties sold after purchase

Legitimate factory-backed extended warranties purchased at the time of a new car purchase can be worthwhile. Third-party extended warranties sold via phone calls, mailers, or pop-up ads after you’ve owned the car for months or years are a different product entirely. These aftermarket warranties frequently contain exclusions so broad that the most common and expensive repairs are not covered. Read the full contract — not the brochure — before signing.

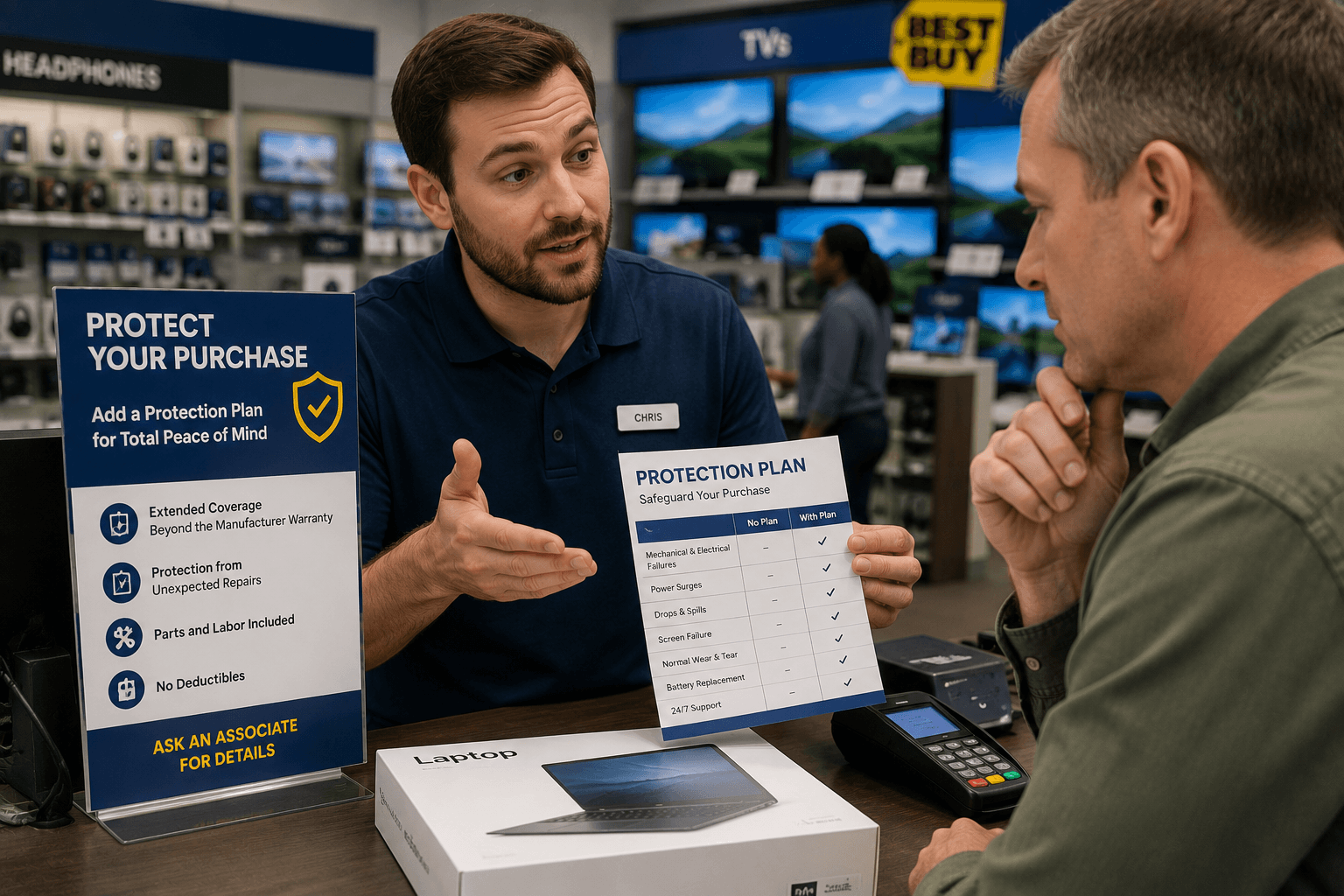

4. Laptop and tablet protection plans

A $1,200 laptop with a $200 three-year protection plan means you’re paying a 17% premium for coverage. Most laptop failures that occur within the protection plan window are covered by the manufacturer’s standard warranty or by your credit card’s purchase protection benefit. Accidental damage coverage — drops and spills — is the only component of most laptop plans that provides value beyond what you already have. If you’re careful with your devices, the plan rarely pays for itself.

5. Furniture and mattress protection plans

Furniture retailers aggressively sell fabric protection plans for $100 to $300 per piece. The plans cover stains, tears, and structural defects — but the exclusion lists are extensive. Normal wear, fading, pet damage, and stains not reported within a specific window are typically excluded. The claim process is frequently described by consumers as deliberately difficult. A $15 can of fabric protector spray applied at home provides most of the stain protection these plans promise.

The general rule: if the cost of the warranty exceeds 15-20% of the product’s price, the warranty is overpriced relative to the risk. Put the money you would have spent on warranties into a savings account. Over time, you’ll come out ahead.